Office building owners face their scariest market in decades. Hybrid work and inflation have upended years of expansion. Flexible work has enabled most companies to downsize or eliminate many offices, while the Fed’s extraordinary interest rate increases have triggered a surge in loan distress. Almost half of U.S. office investments are “underwater.” They are saddled with debt that exceeds their market value. Many investors now teeter on the brink of foreclosure. Most have only two options: Fight their way back to solvency or relinquish their property to their lender.

The fallout will spread well beyond owners and banks. Local economies rely on property investors. Their dollars revitalize downtowns with new amenities, jobs and modern real estate. The tax revenue they generate improves government services. Retirement funds have already suffered lower returns on their office investments. IRAs, 401(k)s, pensions and similar investment vehicles are expected to sustain a further drop in yields.

Many people, even entire communities, feel the effect when real estate investors fail. And right now, failure on a large scale appears inevitable.

Falling lease income

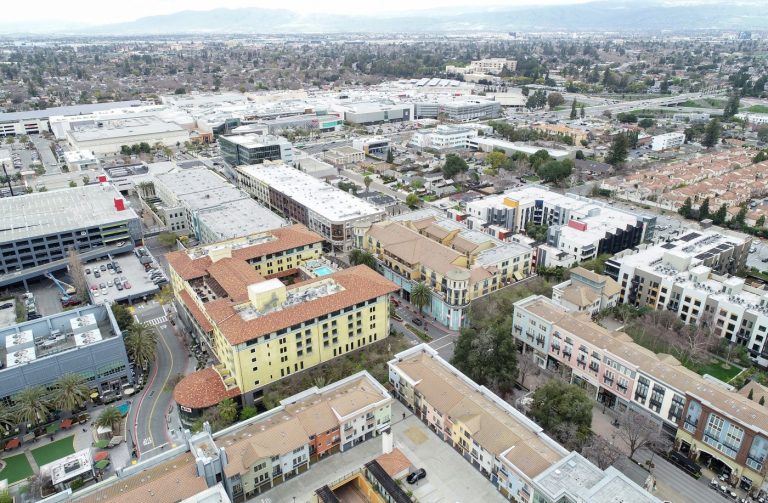

Lease income continues to decline. U.S. office vacancy has reached a record 19.8 percent. The amount of unleased space has climbed past its previous high set more than 40 years ago. In the Bay Area, San Francisco and San Jose have eclipsed the national average with office vacancies above 36% and 35% respectively. Oakland’s first-quarter rate was 19.7%.

Hybrid work policies have driven the rise in discontinued leases. Most companies have leveraged flexible work to shrink their real estate footprint. Many leases have been allowed to expire, and those that are renewed have been cut to half their pre-pandemic size. And the trend lines point down. Offices remain significantly underused, which means corporations will continue to downsize aggressively until they believe their portfolios are optimized.

The reduction in space demand has put intense downward pressure on landlords’ rental income. Asking lease rates appear steady, but the numbers are inflated by owners who wish to avoid reduced property valuations. Landlords are signing deals below their asking rates, and they often seek to draw tenants with longer free rent periods and more generous tenant improvement allowances. True lease rates are substantially lower than what is advertised. The drop in revenue has forced some owners into a deficit. They can no longer afford to fully pay their monthly debt service.

Rising interest rates

Higher interest rates have pushed debtors to the edge. Debt is crucial to real estate investment. Very few properties are purchased entirely with equity.

In response to inflation, the Fed imposed the sharpest interest rate hikes in four decades. That policy ignited a dramatic increase in debt cost, which exposed many property owners to default. At first, most building owners received flexibility. Banks prefer to avoid real estate foreclosure. When rates increased, bankers calculated that it was smarter to forbear some of the interest they were owed to give borrowers a chance to restore profitability.

But lenders have grown impatient and now want to resolve non-performing loans. That pressure puts many investors at risk of default and the loss of their asset. Delinquent payments, missed maturity dates and special servicer transfers have steadily increased over the past 12 months. And the frequency of office building fire sales has risen.

The Fed has promised rate cuts, but they will not arrive in time for many investors. When rates finally do come down, the relief for distressed owners likely will not be sufficient to make their buildings financially stable.

The way through

There is no way around this problem, but there may be a way through. An axiom of investing asserts that capital is most needed when it is least available. That means office building owners will struggle to raise new debt or equity right now. Many owners cannot endure the severity of this market correction, but those who can and wish to maintain ownership of their assets must find a way to reinvest.

Flexible work has remade the traditional use case for an office. Stubbornly low occupancy has proven that post-pandemic workers require an advanced workplace. Corporate leaders have begun to embrace these changes, and landlords should participate. However difficult, if they invest in modern designs and technology to accommodate our new ways of working, owners can improve their bottom line. Amenity-rich properties with spaces that easily reconfigure will lure more tenants. Buildings that provide digital infrastructure to improve onsite experience, facilities management and sustainability will enjoy lower vacancy and higher lease rates.

Related Articles

San Jose apartment complex is bought as Bay Area real estate wobbles

South Bay must build more housing for cutting-edge tech and AI jobs: expert

Grand jury rips county housing agency over San Jose real estate blunder

Downtown Oakland tower is seized by lender as Bay Area office woes widen

$1.6 billion Oakland hospital project gains milestone with key jobs deal

In some cases, an updated design will not be enough — sites must be adapted to a new purpose. Market shifts can reshape a property’s highest and best use. During the condominium boom of the 1980s, many office towers were remodeled into housing. Throughout the dot-com bubble of the late ‘90s, warehouses were repositioned as suburban offices.

Now, in this new world of flexible work, when locations cannot reliably attract office users, owners must convert their buildings to a purpose that is economically viable.

The current downturn has humbled even the most seasoned investors. In the last two years, downtown offices have lost more than 40% of their value. To simply wait for recovery risks an even deeper financial toll. Landlords who wish to survive this crisis must reimagine their properties for a society that has already transformed.

Gabe Burke is a leader in Accenture’s Real Estate & Workplace Solutions consulting practice, which partners with companies to create and implement their post-pandemic real estate strategy.