It’s not a stretch to say that much of California’s economic slowdown can be tied to technology’s tumble.

Let my trusty spreadsheet provide some context by looking inside state-level stats on gross domestic product, a broad measure of business output. Consider the latest reports – the cooldown of 2024’s first quarter and 2023’s last three months – compared with the boom of the previous five years.

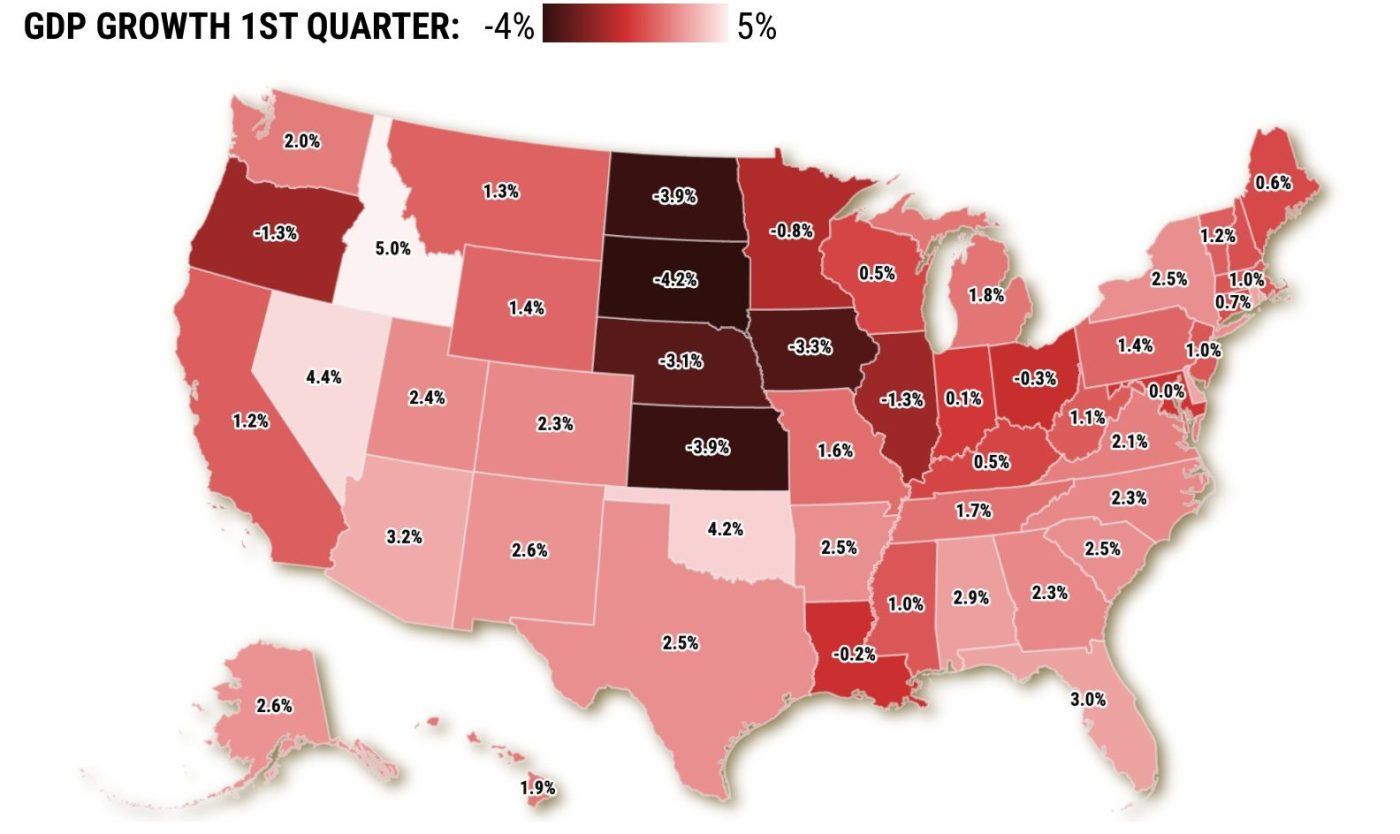

Overall, California’s GDP grew at 2.2% average rate recently vs. its 2019-23 expansion pace of 3.3%. That’s a far bigger swing than the nation: US GDP grew 2.4% in the last two quarters, slightly slower than 2.6% in the previous five years.

Next, ponder the changing roster of what’s powering California’s business climate by focusing on how much key industries add, or subtract, from economic growth.

Let’s look at what’s dubbed “information” – the creator of cutting-edge products and sky-high salaries. This economic slice is dominated by technology firms and also covers groups like Hollywood’s creative talent.

These businesses were expanding at roughly a $35 billion a year pace during California’s five-year economic surge that ended last September. That’s nearly a third of statewide growth. In the last six months, the information sector shrank at a $3 billion annual rate.

Zero surprise. We’ve seen headline-grabbing layoffs at California’s tech giants. Nor has Hollywood production rebounded from labor unrest.

The dark side

Now, ups and downs are nothing new in California’s quirky and dynamic economy. Peek at three other eye-catching tumbles.

Output from California “durable goods” factories – long-lasting stuff from aerospace parts to appliances – grew at an $11 billion-a-year pace in the five-year boom. This year, it’s declining at a $5 billion annual rate over the past two quarters.

The “professional, scientific, and technical” work – high-paying, white-collar jobs – increased at a $21 billion annual pace in the boom, one-fifth of the total. But growth decelerated to $8 billion a year in this recent cooling.

And growth of the “real estate and rental and leasing” segment – folks who facilitate property transactions – shrank by three quarters to $3 billion in the cooldown. High mortgage rates, used by the Federal Reserve to cool the nation’s overheated economy, were key to this chill.

Add it up and this suddenly sluggish quartet of industries collectively increased at a $2 billion a year pace in the last two quarters vs. a $78 billion rate over that five-year boom.

It’s quite a stumble, especially considering these industries create fat paychecks.

The flip side

Related Articles

Bay Area adds jobs in June, but tech-dependent regions lose workers

Prime downtown San Jose spot survives — and thrives — despite COVID woes

Opinion: California faces workforce shortages. It can’t afford to cut training programs

Actually, the job market isn’t so bad for Gen Z college grads

UC Regents OK state-of-the-art $1.49 billion Oakland children’s hospital

How did California grow lately?

Start with government’s contribution to business growth. Those expenditures grew at an $11 billion annual rate in the past two quarters vs. $3 billion in the five-year boom. Hefty budget deficits of numerous California governments, however, suggest this spending spurt will likely be curtailed.

Or look at three industries that may finally be shedding their coronavirus cobwebs.

Retailing’s growth ran at a $16 billion annual rate in the past two quarters – nearly a fifth of the statewide total and almost triple the pace of the five-year boom. Can aggressive shopping by consumers continue to boost the economy – statewide or nationally?

Construction also rebounded, growing at a $10 billion pace the last two quarters. That’s a striking rebound from $2 billion-a-year shrinkage as pandemic limits, plus pricey mortgages, muted production. Massive infrastructure projects – and the state’s thirst for housing – should keep the building trades gainfully employed.

And there’s agriculture, recently growing at a $12 billion annual pace after declining by $2 billion a year. Higher food prices – have you been grocery shopping lately? – can be good for business.

So this reenergized quartet grew at a $49 billion-a-year pace in the last two quarters – almost 10 times the boom’s expansion.

It’s worth noting that these four industries involve less-glamorous and lower-paying work than the aforementioned slumping quartet.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at jlansner@scng.com