U.S. household debt has reached a record and more borrowers are struggling to keep up.

Overall U.S. household debt rose to $17.7 trillion, according to the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit released Tuesday. That’s an increase of $184 billion, or 1.1%, from the fourth quarter.

The data highlight the mounting financial pressures on American families in an age of elevated inflation. The persistent rise in the prices of essentials such as food and rent have strained household budgets, pushing people to borrow against their credit cards to pay for necessities.

Consumers have added $3.4 trillion in debt since the pandemic, and that increased debt bears much higher interest rates.

Total credit card debt stood at $1.12 trillion in the first quarter of 2024, according to the report. That’s down slightly from the $1.13 trillion in the fourth quarter, in line with seasonal patterns of consumers paying debt incurred over the holidays. But credit card balances are up almost 25% from the first quarter of 2020.

“Credit card balances usually rise in the second and third quarters and then they really tend to spike around the holidays in Q4,” Ted Rossman, a senior analyst at Bankrate, wrote in a note to clients. “With inflation and interest rates likely to remain elevated, there’s a very good chance credit card balances will surge to new highs later in 2024.”

Consumers facing a financial squeeze may be maxing out their credit cards and falling behind on payments, Fed researchers said. They noted in a blog post that “one observable factor that is strongly correlated with future delinquencies is a high credit card utilization rate.”

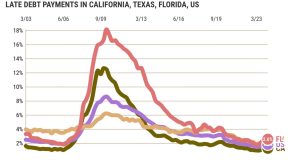

As of March, 3.2% of outstanding debt was in some stage of delinquency. That remains 1.5 percentage points lower than the fourth quarter of 2019, but delinquency transition rates increased for all product types, according to the Fed.

Delinquency woes

In a separate post, economists at the St. Louis Fed pointed out that credit card delinquency rates are returning to historically more normal levels after pandemic-related government assistance programs pushed them to unusually low numbers.

They added, however, that “present levels of credit card delinquency are greater than pre-pandemic levels, suggesting that a trend which began prior to the pandemic has accelerated.”

About 121,000 consumers had a bankruptcy notation added to their credit reports last quarter, and approximately 4.8% of consumers held some debt in third-party collections.

Borrowers using more than 60% of their credit are falling into delinquency at a faster pace than before the pandemic, making up most of the increase in credit card delinquency rates. About a third of balances associated with borrowers using more than 90% of their credit became delinquent in the past year, compared to about 25% before the pandemic.

The data show a wide range in credit card utilization rates. About one in six credit card users are using at least 90% of their available credit. And an additional 11% are using between 60% and 90% of their available credit.

The Fed researchers found younger borrowers and those with lower incomes are more apt to be financially stressed than older borrowers and those with higher incomes, who may have more credit available. “Millennials were the only group whose delinquencies exceeded their pre-pandemic rate,” New York Fed researchers wrote in a blog post.

The Fed’s report showed 6.9% of credit card debt transitioned to serious delinquency last quarter, up from 4.6% a year ago. And for credit card holders aged 18–29, 9.9% of balances were in serious delinquency.

“In the first quarter of 2024, credit card and auto loan transition rates into serious delinquency continued to rise across all age groups,” said Joelle Scally, Regional Economic Principal within the Household and Public Policy Research Division at the New York Fed. “An increasing number of borrowers missed credit card payments, revealing worsening financial distress among some households.”

Auto loan delinquencies are also higher as the average monthly car payment jumped to $738 in 2023. Close to 2.8% of auto loans are now 90 or more days delinquent — that equates to more than 3 million cars. Auto loans are the second-largest debt category following mortgage debt, with $1.62 trillion outstanding.

The biggest household debt holding is for housing. It accounts for more that 70% of the total. That debt is performing well, but homeowners are increasingly tapping their accumulated home equity in the form of a home equity loans.

Last quarter $16 billion in additional home equity loans was originated — the biggest increase since 2008 — and $37 billion was added over the past year. Homeowners have about $580 billion in outstanding home equity credit available, the most in about 15 years.

Outstanding student loan debt was roughly unchanged and stood at $1.60 trillion. Its difficult to determine how much of that debt is delinquent as missed federal student loan payments will not be reported to credit bureaus until the fourth quarter.

___

©2024 Bloomberg L.P. Visit bloomberg.com. Distributed by Tribune Content Agency, LLC.