Californians started 2024 with the most challenges in paying their bills on time in nine quarters.

If there’s a must-watch number out there to gauge the financial pulse of the consumer, it’s the New York Fed’s quarterly tracking of who’s paying their bills on time. These figures are compiled from an analysis of credit histories from Equifax. So, we’re talking about bill-paying patterns of folks with credit profiles.

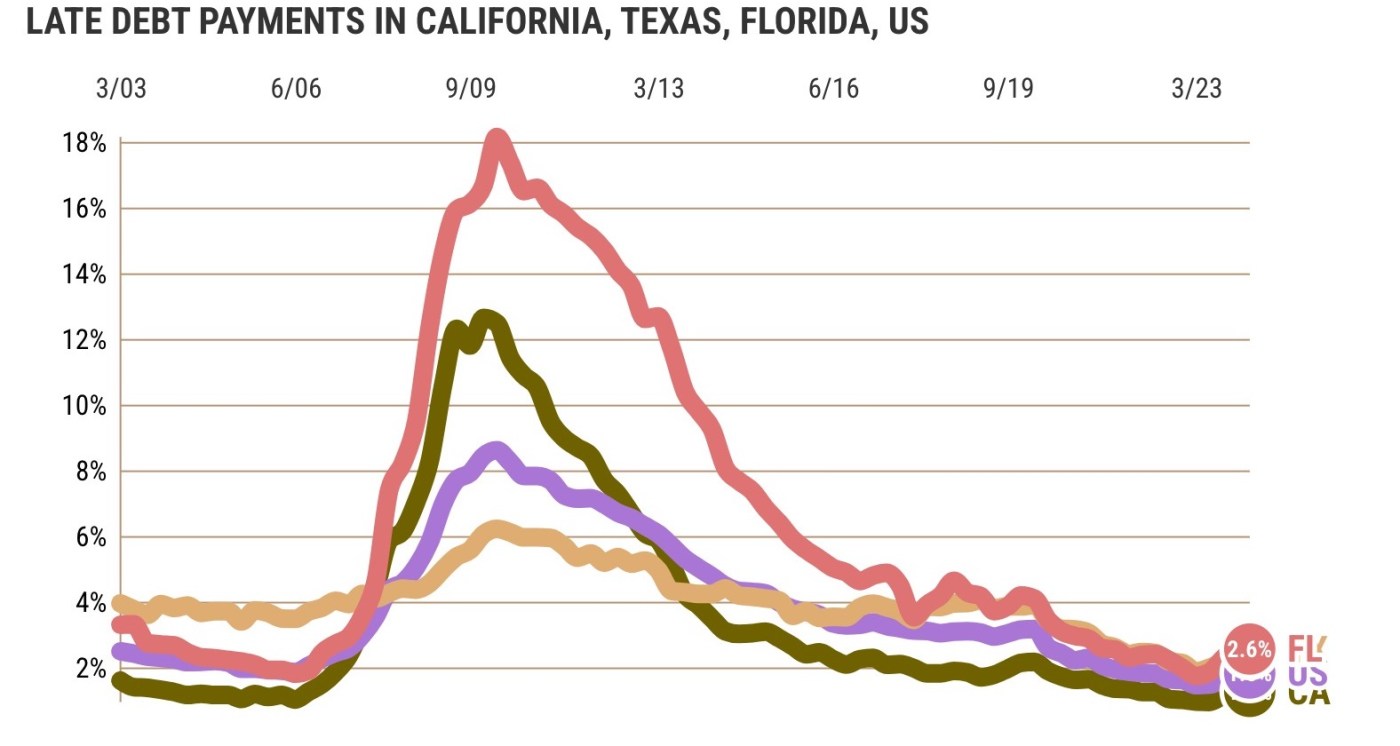

Caveat noted, we see that Californians had 1.27% of their balances marked late by 90 days or more. That’s the highest delinquency rate since 2021’s fourth quarter, when the economy was digesting both pandemic business shutdowns and a flood of stimulus dollars. And late payers are also up from 0.96% at 2023’s start.

But before you sound any big alarms, here’s a little perspective: This current pace of tardy payments is well below the 1.87% average of pre-coronavirus 2018-19. Or, what we call the normal days.

Plus, it’s nowhere near the Great Recession’s peak of 12.6% delinquency in 2009’s 4th quarter. Or, what we call the worst-case scenario.

And this may surprise you, too: Californians are paying bills far swifter than their national peers and even their economic arch-rivals, Texans and Floridians.

Nationally, 1.83% of bills were plus-90 days late in the first quarter vs. 1.46% a year ago. As with California, early 2024’s late payers are below the 3.07% seen in 2018-19 and the 8.6% peak of 2010’s 1st quarter.

In Texas, 2.53% of bills were plus-90-days late vs. 1.9% a year ago and 3.9% in 2018-19. The peak was 6.2% in 2010’s 1st quarter. And in Florida, delinquency ran 2.56% vs. 1.74% a year ago and 4.1% in 2018-19. That peak ran 18.2% in 2010’s 1st quarter.

So, to varying degrees, the national and statewide patterns are aligned: Skipped bills are rising yet still below pre-pandemic days.

Bunch of debts

What’s likely no surprise is how much Californians owe – a bunch, and that’s primarily due to the state’s expensive housing.

California consumer debts equaled $86,940 per capita in the first quarter, with 80% of that debt tied to mortgages. That’s up 2.2% in a year and 21% in five years.

Compare that with the typical American’s debts: $61,874 – 70% in mortgages – which is up 2.7% in a year and 22% in five years.

The Golden State’s economic arch-rivals have even fewer debts, but borrowing has been surging. Tough question: Is that economic confidence, or is the cash needed to cover unpaid bills?

Texas debts run $57,450 per capita – 65% in mortgages – up 3.4% in a year and 31% in five years. In Florida, it’s $60,590 – 68% in mortgages – was up 5.1% in a year and 32% in five years.

Mortgage making

Related Articles

Bay Area consumer prices hop higher as pace of inflation worsens

Bay Area small businesses struggle with inflation as optimism slides

Many PG&E customers could see higher bills after state OKs new monthly utility fee

CPUC voting soon on $24 fixed monthly charge for California electricity bills

Brooks: Why are we gambling with America’s future on national debt?

Since we all suffer some degree of bubble-bursting PTSD, a first question may be: “Are most house payments being paid?”

Yes, but 0.33% of California mortgage debts were plus-90 days late in the first quarter — up from 0.19% a year earlier. But this delinquency rate is down from 0.52% in 2018-19 and just a sliver of the 13.2% pinnacle in 2009’s fourth quarter.

Again, California outshines the competition.

US mortgage delinquency ran 0.6% in the quarter vs. 0.44% a year ago and 1.05% in 2018-19. The peak was 8.9% in 2010’s first quarter.

Texas’ late mortgages were 0.63% to start 2024 – almost double 0.32% a year ago – but off from 0.79% in 2018-19. Slow-paying mortgages in Florida ran 1% – triple 0.32% a year ago – but were off the 1.71% rate of 2018-19.

Foreclosures, the really troublesome home loan indicator – are a rarity

Going broke

Perhaps the worst cases of skipping bills – bankruptcy filings – also have been rare so far in this economic cycle.

New bankruptcies in California ran at 10 per 100,000 people to start 2024. That’s up from eight a year ago but down from 16 in 2018-19 and 500 at the peak of 2009’s 2nd quarter.

US bankruptcies ran at 15 per 100,000 in the first quarter vs. 13 year ago and 26 in 2018-19. The peak was 240 in 2009’s second quarter.

Texas started 2024 with 14 new bankruptcies per 100,000 vs. 12 in 2023’s first quarter and 22 in 2018-19. Florida had 18 per 100,000 – double nine from a year ago but off from 29 in 2018-19.

Bottom line

US consumers started last year with record low late payments on this New York Fed scorecard, which dates to 2003. Same for Texans and Floridians.

California’s skipped bills hit their bottom in 2023’s second quarter.

So, an uptick from best-ever payment habits seemed inevitable, especially when the Federal Reserve has been hiking interest rates to chill an overheated economy suffering a bad bout of inflation.

Still, increased late payments can’t be ignored. The past year’s surge is something to keep a keen eye on.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at jlansner@scng.com